Advising Clients on College Funding and Student Loan Debt

As the cost of higher education continues to soar, college funding has become a pressing concern for both students and their families. As a financial advisor, one of the most significant challenges you may encounter is helping clients prepare for and manage the expenses associated with a college education. In this article, we’ll explore the aspects of advising clients on college funding and student loan debt, equipping you with the knowledge to assist your clients in making informed decisions while achieving their educational goals.

Understanding the Landscape of College Funding

The rising cost of higher education has become a major concern for families across the country. As a financial advisor, it’s essential to have a firm grasp of the evolving landscape of college costs and funding options available.

1. Assessing Clients’ College Savings and Investment Options

Start by evaluating your clients’ current college savings and investment vehicles. Encourage them to consider 529 plans, which offer tax advantages and flexibility for education expenses. Explain the benefits of these plans, including tax-free withdrawals and potential state tax deductions.

Discuss the different types of 529 plans available and how they align with your clients’ goals and risk tolerance. For instance, direct-sold plans are typically more affordable, while advisor-sold plans offer professional guidance for a higher cost.

2. Exploring Other Funding Sources

In addition to 529 plans, explore alternative funding sources with your clients. Discuss the merits of custodial accounts and Coverdell Education Savings Accounts (ESAs). Custodial accounts, also known as UTMA or UGMA accounts, can offer flexibility but may have tax implications to consider. ESAs, on the other hand, have more restrictions on contributions but provide tax-free withdrawals for qualified education expenses.

Additionally, consider the possibility of strategic withdrawals from retirement accounts, such as Roth IRAs, if your clients are approaching retirement age and need extra funds for their child’s education. This strategy requires careful planning to balance retirement savings with college funding.

3. Financial Aid and FAFSA

Ensure that your clients understand the significance of completing the Free Application for Federal Student Aid (FAFSA) early. This form determines eligibility for federal and state grants, work-study programs, and federal student loans. Provide guidance on the financial aid process and help your clients navigate different aid packages.

Explain the difference between need-based and merit-based aid and how students can qualify for each. Emphasize the importance of submitting the FAFSA as soon as possible after October 1st of the student’s senior year in high school, as some financial aid is awarded on a first-come, first-served basis.

Strategizing to Minimize Student Loan Debt

Student loan debt can be a significant burden for recent graduates, affecting their long-term financial well-being. As advisors, you play a crucial role in helping your clients minimize their student loan debt.

1. Encourage Informed College Choices

Guide your clients and their children in making informed decisions about college choices. Advise them on finding schools that align with their educational and financial goals while offering scholarships, grants, and work-study opportunities that can help reduce the need for loans.

Encourage students to apply for a mix of reach, match, and safety schools. Reach schools are those with higher acceptance criteria, match schools are those where the student’s academic profile aligns with the school’s average admitted student, and safety schools are those where the student’s academic profile exceeds the school’s average admitted student. A mix of these types of schools can provide a range of financial aid offers, giving your clients more options.

2. Understand Loan Types and Terms

Educate your clients on the different types of student loans available, including federal subsidized and unsubsidized loans, PLUS loans, and private loans. Explain the terms, interest rates, and repayment options associated with each loan type to help your clients make informed borrowing decisions.

Federal loans often offer more favorable terms and flexible repayment options compared to private loans. For example, federal loans offer income-driven repayment plans, deferment, and forbearance options during financial hardships.

3. Explore Loan Repayment Strategies

Discuss different loan repayment strategies with your clients. This might include income-driven repayment plans, loan forgiveness programs for certain professions, or refinancing options to secure more favorable interest rates. Tailor the approach to each client’s unique financial situation and long-term goals.

Income-driven repayment plans adjust monthly payments based on a borrower’s income and family size. These plans can be particularly helpful for graduates who have lower starting salaries or face financial difficulties after graduation.

Loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF), can provide a light at the end of the tunnel for borrowers working in certain public service fields. Ensure your clients understand the eligibility criteria and follow the necessary steps to qualify for loan forgiveness.

4. Assess Post-Graduation Financial Planning

Help your clients develop a post-graduation financial plan that accounts for student loan repayment. Encourage them to live within their means and allocate funds toward loan repayment while still saving for emergencies, retirement, and other financial goals.

Creating a Comprehensive College Funding Strategy

To provide holistic advice on college funding and student loan debt, consider creating a comprehensive strategy that addresses both short-term and long-term financial goals.

1. Develop a Customized College Funding Plan

Work with each client individually to create a customized college funding plan that aligns with their financial situation and goals. Consider factors such as income, existing savings, family size, and time horizon for college expenses.

2. Forecasting Future College Costs

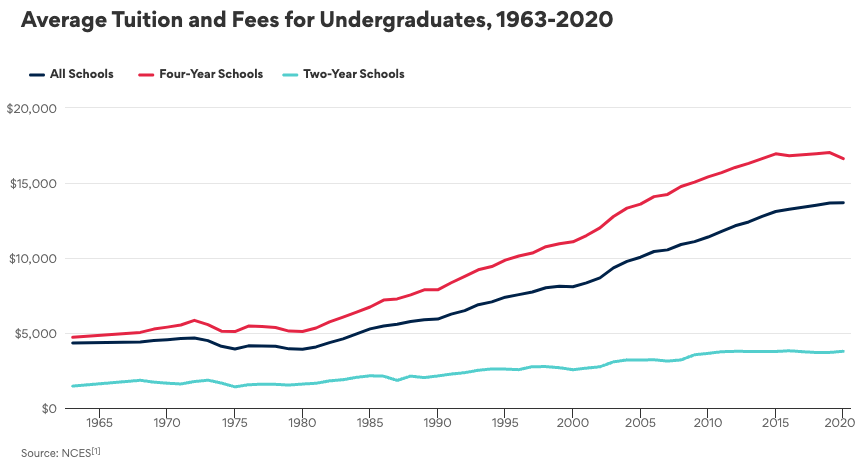

Help your clients anticipate future college costs based on the inflation rate of college tuition. The cost of tuition alone has more than tripled since the 1960s.1 Across all types of schools, the cost of college has increased more than 143% since 1963.1 Forecasting potential expenses allow your clients to set realistic savings goals and adjust their strategy as necessary.

3. Emphasize the Importance of Saving Early

Stress the significance of starting college savings as early as possible. The power of compounding can significantly impact savings over time, making early contributions more valuable in the long run.

4. Regularly Review and Adjust the Plan

Encourage clients to regularly review and adjust their college funding plan. Life circumstances and financial situations change, and flexibility is essential in adapting to new challenges and opportunities.

The Bottom Line

As a financial advisor, guiding your clients through the maze of college funding and student loan debt is an invaluable service. By understanding the landscape of college costs, exploring funding options, and providing expert advice on minimizing student loan debt, you can empower your clients to make informed choices and achieve their educational aspirations without compromising their financial future. Remember that a comprehensive approach, tailored to each client’s unique situation, is key to creating a successful college funding strategy. Your clients will thank you for helping them make smart financial decisions that lead to a brighter educational future